Your loan got rejected. Or you haven’t applied because you don’t have a project report.

Either way, you are stuck. And you are losing money every single day.

Every day you wait to apply for your Mudra loan:

- Your competitor buys that stock you wanted

- Your customer goes to someone else

- Your shop stays smaller than it should be

- Your family waits longer for a better life

Stop waiting.

Here is the truth that CAs do not want you to know:

You do not need to pay ₹5,000-10,000 for a project report.

You do not need to wait 3-5 days.

You do not need to understand DSCR or MPBF or balance sheets.

You need 7 simple steps. Answer simple questions about your business. And in just 30 minutes you will get your project report for mudra loan .

QUICK SUMMARY – 7 STEPS TO MAKE A PROJECT REPORT (30 SECOND READ)

| Step | What You Do | Time Required | Why It Matters |

|---|---|---|---|

| 1 | Write Executive Summary | 10 minutes | Bank officer spends 30 seconds here – make it count |

| 2 | Fill Business & Promoter Profile | 5 minutes | Proves you know this business |

| 3 | Write Market Analysis | 10 minutes | Shows customers exist |

| 4 | List Operational Plan & Assets | 10 minutes | Shows exactly where loan money goes |

| 5 | Calculate Project Cost & Means of Finance | 5 minutes | Shows your own contribution (5-10%) |

| 6 | Create Financial Projections (P&L, Balance Sheet, Cash Flow) | 20 minutes | Proves you can repay the loan |

| 7 | Calculate DSCR (Debt Service Coverage Ratio) | 5 minutes | The single most important number – must be above 1.25 |

Total time to make a project report manually: ~65 minutes (plus learning curve)

Total time using MudraReady: 15 minutes (no learning curve, no calculations)

👉 [Skip the manual work – make your report in 30 minutes here]

This guide gives you both.

| If you are… | This guide will help you… |

|---|---|

| An existing business owner (like Ramesh, who we will meet) | Show past performance + future projections |

| A new business owner (like Priya, who we will meet) | Show establishment plan + future projections |

| Any business owner who needs a Mudra loan | Make a bank-ready project report in 7 steps |

By the time you finish reading, you will have a bank-ready project report. Or you will know exactly how to get one in 30 minutes.

Let me show you how.

*– Written by the MudraReady team. We have visited 15+ bank branches across UP, Bihar, and Punjab. We have sat across from loan officers at SBI, PNB, and Bank of Baroda. We asked them directly: “What makes you approve a project report?” Their answers are inside this guide.*

CHAPTER 1: WHAT IS A PROJECT REPORT? (SIMPLEST EXPLANATION YOU WILL FIND)

A project report is your business’s resume.

When you apply for a job, you submit a resume. It tells the employer who you are, what you have done, and why they should hire you.

A project report does the same thing for your loan.

| Resume Section | Project Report Section |

|---|---|

| Your name and contact | Business name and address |

| Your work experience | Promoter experience and qualifications |

| Your achievements | Past business performance or establishment plan |

| Your future goals | Financial projections for 3-5 years |

| Why they should hire you | DSCR (can you pay the EMI?) |

Banks receive thousands of loan applications. They cannot talk to every applicant for hours.

They read your project report. If it is good, they approve. If it is bad, they reject.

That is all. That is what a project report is.

📌 WHY THIS MATTERS: A good project report = loan approved. A bad project report = loan rejected. 45% of Mudra loans get rejected. The number one reason? A weak project report. Do not be that statistic.

CHAPTER 2: IS PROJECT REPORT MANDATORY FOR MUDRA LOAN?

The answer depends on which loan category you are applying for.

| Category | Loan Amount | Project Report Required? |

|---|---|---|

| Shishu | Up to ₹50,000 | No (but helpful) |

| Kishore | ₹50,001 – ₹5,00,000 | YES – MANDATORY |

| Tarun | ₹5,00,001 – ₹10,00,000 | YES – MANDATORY |

| Tarun Plus | ₹10,00,001 – ₹20,00,000 | YES – MANDATORY (detailed) |

⚠️ STOP. IF YOU ARE APPLYING FOR KISHORE, TARUN, OR TARUN PLUS: Do not go to the bank without a project report. They will not even look at your application. Save yourself the trip. Get your Project Report first.

CHAPTER 3: 5 THINGS BANKS CHECK IN YOUR PROJECT REPORT (BANKER INSIDER INFO)

We sat across from loan officers at SBI, PNB, and Bank of Baroda. We asked them: “What do you check first?”

Here is exactly what they said.

| What Banks Check | Why It Matters | What Happens If It Is Wrong |

|---|---|---|

| DSCR (Debt Service Coverage Ratio) | “Can you pay the EMI every month?” | Below 1.25 = automatic rejection. They do not read the rest. |

| MPBF (Working Capital) | “Do you understand your daily cash needs?” | Wrong calculation = they think you do not understand your business. |

| Promoter Experience | “Have you run this type of business before?” | No experience = they worry you will fail. |

| Realistic Projections | “Are your numbers honest or are you lying?” | 200% growth in Year 1 = they laugh and reject. |

| Complete Documentation | “Did you bother to fill every section?” | Missing sections = they think you are careless. |

📌 INSIDER TIP: An SBI branch manager in Lucknow told me: “I open the file, go straight to the DSCR page. If it is missing or below 1.25, I close the file. I do not look at anything else. I do not have time.”

CHAPTER 4: THE 7 STEPS TO MAKE A PROJECT REPORT

Step 1: The One Page That Decides Your Loan – Executive Summary

The executive summary is the first page of your project report. It is also the most important page.

Bank officers spend 30 seconds on your executive summary. If it is clear, they read the rest. If it is messy, they put your file aside.

What to include in your executive summary:

| Field | What to Write | Example |

|---|---|---|

| Business Name | Your shop/business name | Ramesh Kirana Store |

| Owner Name | Your full name | Ramesh Kumar Gupta |

| Business Address | Complete address | Shop No. 15, Main Market, Mani Majra, Chandigarh |

| Loan Amount | How much you need | ₹2,00,000 |

| Loan Purpose | What you will use the money for | Working capital and stock purchase |

| Annual Revenue (Projected) | Your expected yearly sales | ₹9,60,000 |

| Net Profit After Tax (Year 1) | Your expected yearly profit | ₹68,575 |

| DSCR (Year 1) | Your debt service coverage ratio | 2.00 |

| Loan Tenure | How many years to repay | 5 years |

Sample Executive Summary Table:

| Field | Value |

|---|---|

| Business Name | Ramesh Kirana Store |

| Owner Name | Ramesh Kumar Gupta |

| Business Address | Shop No. 15, Main Market, Mani Majra, Chandigarh |

| Loan Amount | ₹2,00,000 |

| Loan Purpose | Working capital and stock purchase |

| Annual Revenue (Projected) | ₹9,60,000 |

| Net Profit After Tax (Year 1) | ₹68,575 |

| DSCR (Year 1) | 2.00 |

| Loan Tenure | 5 Years |

📌 WHY THIS MATTERS: The bank officer has 100 files on their desk. Your executive summary is your only chance to grab their attention. Make it count.

Ready for the next step? Keep reading.

Step 2: Business & Promoter Profile – Who You Are And Why Banks Should Trust You

This section tells the bank two things: what your business is, and who is running it.

Part A: Business Information

| Field | What to Write | Example (Existing Business) | Example (New Business) |

|---|---|---|---|

| Business Name | Your shop/business name | Ramesh Kirana Store | Priya Beauty Parlour |

| Nature of Business | What do you sell? | Retail – Kirana / General Store | Service – Beauty Parlour / Salon |

| Business Address | Complete address | Shop No. 15, Main Market, Mani Majra, Chandigarh | Shop No. 8, Sector 12, Indira Nagar, Lucknow |

| Business Status | New or existing? | Existing Business | New Business |

| Constitution | Legal structure | Proprietorship | Proprietorship |

| Number of Employees | Total staff including owner | 2 | 1 (owner only) |

| Years in Business | How long have you been running? | 3 years (since May 2023) | 0 (new business) |

For existing businesses (like Ramesh):

Write your actual numbers. Be honest. If you have been running for 2 years, write 2 years. Do not exaggerate.

For new businesses (like Priya):

Write “New Business (to be established)” in the Business Status field. For years in business, write “0”. You will focus on your establishment plan instead of past performance.

Part B: Promoter Information

| Field | What to Write | Example |

|---|---|---|

| Promoter Name | Your full name (exactly as per Aadhaar) | Ramesh Kumar Gupta |

| Father’s Name | Your father’s full name | Rajesh Kumar Gupta |

| Date of Birth | Your DOB | 15 March 1992 |

| Age | Your age | 34 years |

| Gender | Male/Female/Other | Male |

| Education | Your highest qualification | 12th Pass |

| Experience | Your relevant business experience | 5 years working in uncle’s kirana store |

| Social Category | General/OBC/SC/ST | General |

⚠️ IMPORTANT: Your name on the project report MUST match your Aadhaar card exactly. If your Aadhaar says “Ramesh Kumar Gupta” but you write “Ramesh K Gupta”, the bank will reject your application. Banks are strict about this.

Why banks care about promoter experience:

| If you have experience | The bank thinks | If you have no experience | The bank thinks |

|---|---|---|---|

| “This person knows this business” | Lower risk | “This person is guessing” | Higher risk |

| “They will likely succeed” | Approve faster | “They might fail” | More scrutiny |

📌 INSIDER TIP: A PNB branch manager in Patna told me: “If someone applies for a restaurant loan but has never worked in a restaurant, I am very careful. If someone applies for a tailoring loan and has been stitching for 10 years, I approve faster. Experience matters.”

Ready for the next step? Keep reading.

Step 3: Market Analysis – Proving Customers Will Come

This section tells the bank that people will actually buy from you.

Banks have approved loans for businesses that failed because there was no demand. They do not want to make that mistake again.

What to include in your market analysis:

| Topic | What to Write | Example (Kirana Store) |

|---|---|---|

| Target Customers | Who will buy from you? | Local residents, daily wage workers, families in surrounding colonies |

| Customer Base Size | How many potential customers? | Approximately 5,000 households within 1 km radius |

| Competitors | Who else sells similar products? | 2 existing kirana stores |

| Your Advantage | Why will customers choose you? | Better location, longer hours, home delivery |

| Location Advantage | Why is your location good? | High-footfall residential area, no large competitors nearby |

Sample Market Analysis Paragraph (Existing Business – Ramesh):

“Ramesh Kirana Store is located in Mani Majra, Chandigarh. The area has approximately 5,000 households. Currently, 2 kirana stores serve this population. Both close by 9 PM. Ramesh’s store will remain open until 10 PM. He will also offer free home delivery for orders above ₹500. Based on his 3 years of experience, he knows that customers value convenience over price. He expects to capture 30% of the local market within Year 1.”

Sample Market Analysis Paragraph (New Business – Priya):

*”Priya Beauty Parlour will open in Sector 12, Indira Nagar, Lucknow. This area has 3 housing societies with 2,000+ families. Currently, only 1 small parlour operates here. It has a waiting time of 2-3 days for appointments. Priya has surveyed 50 women in the area. 42 said they would switch to a new parlour if it offered better service and lower prices. Priya will offer a 20% discount for the first month to attract customers.”*

📌 WHY THIS MATTERS: Banks want proof that customers exist. If you cannot explain who will buy from you, the bank will assume no one will.

Ready for the next step? Keep reading.

Step 4: Operational Plan – How You Will Run Your Business Day To Day

This section tells the bank exactly how you will spend their money.

What to include:

| Topic | What to Write | Example |

|---|---|---|

| Location | Where is your shop? | Main Market, Mani Majra, Chandigarh |

| Shop Size | How many square feet? | 400 sq. ft. |

| Shop Ownership | Rented or owned? | Rented (₹5,000 per month) |

| Operating Hours | When will you be open? | 8 AM to 10 PM (14 hours daily) |

| Suppliers | Where will you buy stock? | Local wholesalers in Sector 20, Chandigarh |

Assets Table – What You Will Buy With The Loan:

| Asset | Cost (₹) |

|---|---|

| Shop Interior / Racks / Shelving | 40,000 |

| Furniture & Fittings | 15,000 |

| POS & Billing System | 10,000 |

| Weighing Scale & Storage Containers | 5,000 |

| Initial Stock Purchase | 1,20,000 |

| Working Capital Buffer | 10,000 |

| Total Project Cost | 2,00,000 |

⚠️ For new businesses: If you are starting from zero, your asset list will be similar. The only difference is that you will not have past stock. Your “Initial Stock Purchase” will be higher because you are buying everything for the first time. That is normal. Banks expect this.

Why banks want to see this table:

| If you show a detailed asset list | The bank thinks |

|---|---|

| “They know exactly where our money is going” | Low risk |

| “They have thought this through” | Approve faster |

| If you do not show a detailed asset list | The bank thinks |

|---|---|

| “They do not know how to use our money” | High risk |

| “They are not serious” | Likely reject |

📌 INSIDER TIP: A Bank of Baroda branch manager in Jaipur told me: “I have seen applications where the applicant asks for ₹5 lakh but writes ‘business expenses’ as the only line item. I reject those immediately. If they cannot tell me where the money is going, I cannot approve.”

Ready for the next step? Keep reading.

Step 5: Project Cost & Means Of Finance – Where The Money Comes From

This section tells the bank the total cost of your project and how much you are contributing.

Project Cost Table:

| Particulars | Amount (₹) |

|---|---|

| Fixed Assets (Interior + Furniture + Equipment) | 70,000 |

| Initial Stock Purchase | 1,20,000 |

| Working Capital Buffer | 10,000 |

| Total Project Cost | 2,00,000 |

Means of Finance Table:

| Source | Amount (₹) | Percentage |

|---|---|---|

| Promoter’s Contribution (Your Own Money) | 10,000 | 5% |

| Mudra Loan (Bank Loan) | 1,90,000 | 95% |

| Total | 2,00,000 | 100% |

⚠️ STOP. READ THIS.

Many applicants think: “Mudra loan is government loan. They will give me 100%. I do not need to put my own money.”

Wrong.

| Loan Amount | Minimum Own Contribution Expected |

|---|---|

| Below ₹2,00,000 | 5-10% |

| ₹2,00,000 – ₹5,00,000 | 10-15% |

| Above ₹5,00,000 | 15-20% |

Banks want to see that you have skin in the game. If you are not willing to invest your own money, why should the bank?

📌 INSIDER TIP: An SBI branch manager in Varanasi told me: “If someone asks for a ₹10 lakh loan but has saved nothing themselves, I wonder – what were they doing all these years? Why do they need 100% from us? It is a red flag.”

For new businesses: Your own contribution can come from savings, family support, or borrowing from friends. Show proof (bank statement showing the amount). Even ₹10,000 on a ₹2 lakh loan is acceptable.

Ready for the next step? Keep reading.

Step 6: Financial Projections – Will You Make Enough Profit To Pay The EMI?

This is the most important section of your project report. The bank wants to see numbers.

But here is the problem: Most business owners do not know how to make financial projections. CAs charge ₹5,000 for this. You do not need to pay that.

Let me show you how to do it yourself.

Step 6.1: Estimate Your Monthly Sales

| Business Type | Realistic Monthly Sales Range |

|---|---|

| Kirana Store | ₹80,000 – ₹2,50,000 |

| Beauty Parlour | ₹25,000 – ₹60,000 |

| Tailoring Shop | ₹15,000 – ₹40,000 |

| Auto Rickshaw | ₹25,000 – ₹40,000 |

| Dairy Farm | ₹50,000 – ₹1,50,000 |

| Restaurant / Dhaba | ₹1,00,000 – ₹4,00,000 |

For existing businesses (Ramesh): Use your actual monthly sales from the last 6-12 months. Do not exaggerate.

For new businesses (Priya): Estimate based on market research. Talk to 10-15 potential customers. Ask them: “How much would you spend at my shop per month?” Take the average. Be realistic.

Step 6.2: Calculate Your Annual Sales

Annual Sales = Monthly Sales × 12 × Capacity Utilization (Year 1)

| Year | Capacity Utilization | Why |

|---|---|---|

| Year 1 | 70% | New businesses take time to ramp up |

| Year 2 | 90% | You gain customers |

| Year 3-5 | 100% | Full capacity |

Example (Ramesh Kirana Store):

| Year | Monthly Sales | ×12 | Capacity | Annual Sales |

|---|---|---|---|---|

| Year 1 | 80,000 | 9,60,000 | 70% | 9,60,000 |

| Year 2 | 88,000 | 10,56,000 | 90% | 10,56,000 |

| Year 3 | 95,000 | 11,40,480 | 100% | 11,40,480 |

| Year 4 | 1,00,000 | 12,08,909 | 100% | 12,08,909 |

| Year 5 | 1,04,000 | 12,58,589 | 100% | 12,58,589 |

Step 6.3: Calculate Your Gross Profit

Gross Profit = Annual Sales – Cost of Goods Sold (COGS)

| Business Type | Typical COGS Percentage |

|---|---|

| Kirana Store | 70-80% |

| Beauty Parlour | 30-40% |

| Tailoring Shop | 35-45% |

| Restaurant | 60-70% |

| Dairy Farm | 65-75% |

Example (Ramesh Kirana Store with 75% COGS):

| Year | Annual Sales | COGS (75%) | Gross Profit |

|---|---|---|---|

| Year 1 | 9,60,000 | 7,20,000 | 2,40,000 |

| Year 2 | 10,56,000 | 7,92,000 | 2,64,000 |

| Year 3 | 11,40,480 | 8,55,360 | 2,85,120 |

| Year 4 | 12,08,909 | 9,06,682 | 3,02,227 |

| Year 5 | 12,58,589 | 9,43,942 | 3,14,647 |

Step 6.4: Calculate Your Operating Expenses

| Expense | Monthly | Annual |

|---|---|---|

| Rent | 5,000 | 60,000 |

| Electricity | 2,000 | 24,000 |

| Salary (total staff) | 3,000 | 36,000 |

| Miscellaneous | 2,000 | 24,000 |

| Total | 12,000 | 1,44,000 |

Step 6.5: Calculate Your Net Profit

Net Profit = Gross Profit – Operating Expenses – Interest – Depreciation

Complete P&L Statement – 5 Years (Ramesh Kirana Store):

| Particulars | Year 1 (₹) | Year 2 (₹) | Year 3 (₹) | Year 4 (₹) | Year 5 (₹) |

|---|---|---|---|---|---|

| Annual Sales | 9,60,000 | 10,56,000 | 11,40,480 | 12,08,909 | 12,58,589 |

| Less: COGS (75%) | 7,20,000 | 7,92,000 | 8,55,360 | 9,06,682 | 9,43,942 |

| Gross Profit | 2,40,000 | 2,64,000 | 2,85,120 | 3,02,227 | 3,14,647 |

| Less: Operating Exp. | 1,44,000 | 1,51,200 | 1,58,760 | 1,66,698 | 1,75,033 |

| EBIT | 96,000 | 1,12,800 | 1,26,360 | 1,35,529 | 1,39,614 |

| Less: Interest (10.75%) | 20,425 | 17,463 | 13,670 | 9,205 | 4,140 |

| Less: Depreciation (10%) | 7,000 | 6,300 | 5,670 | 5,103 | 4,593 |

| Net Profit After Tax | 68,575 | 89,037 | 1,07,020 | 1,21,221 | 1,30,881 |

📌 WHAT THIS TABLE TELLS THE BANK: “This business makes profit every year. The profit grows over time. The profit is higher than the EMI (₹48,000/year). This loan is safe.”

Ready for the next step? Keep reading.

Step 7: DSCR – The Number That Decides Your Loan

DSCR stands for Debt Service Coverage Ratio.

In simple words: DSCR tells the bank whether your business earns enough money to pay the EMI every month.

The DSCR Formula:

DSCR = (Net Profit + Depreciation + Interest on Loan) ÷ Annual EMI

Example Calculation (Ramesh Kirana Store, Year 1):

| Component | Amount (₹) |

|---|---|

| Net Profit After Tax | 68,575 |

| Add: Depreciation | 7,000 |

| Add: Interest on Loan | 20,425 |

| Total Available for Debt Service | 96,000 |

| Annual EMI (₹4,000 × 12) | 48,000 |

| DSCR | 2.00 |

What This DSCR Means:

| DSCR | Meaning | Bank Decision |

|---|---|---|

| Below 1.00 | You cannot pay the full EMI | Reject immediately |

| 1.00 – 1.24 | You can pay but no safety margin | Likely reject |

| 1.25 – 1.49 | You can pay with small safety margin | Accept |

| 1.50 – 2.00 | Strong repayment capacity | Accept |

| 2.00 (Ramesh’s DSCR) | Very strong – earns 2x the EMI | Fast approval |

DSCR – 5 Year Projection (Ramesh Kirana Store):

| Year | Net Profit (₹) | Depreciation (₹) | Interest (₹) | Total (₹) | Annual EMI (₹) | DSCR |

|---|---|---|---|---|---|---|

| 1 | 68,575 | 7,000 | 20,425 | 96,000 | 48,000 | 2.00 |

| 2 | 89,037 | 6,300 | 17,463 | 1,12,800 | 48,000 | 2.35 |

| 3 | 1,07,020 | 5,670 | 13,670 | 1,26,360 | 48,000 | 2.63 |

| 4 | 1,21,221 | 5,103 | 9,205 | 1,35,529 | 48,000 | 2.82 |

| 5 | 1,30,881 | 4,593 | 4,140 | 1,39,614 | 48,000 | 2.91 |

⚠️ STOP. IF YOUR DSCR IS BELOW 1.25, FIX IT BEFORE SUBMITTING.

| If your DSCR is below 1.25 | How to fix it |

|---|---|

| Increase your sales projection | Add 10% more customers |

| Reduce your expense projection | Find cheaper rent or reduce staff cost |

| Reduce your loan amount | Borrow less, contribute more from savings |

| Increase your loan tenure | Longer tenure = lower EMI = higher DSCR |

📌 INSIDER TIP: An SBI branch manager in Lucknow told me: “I open the file, go straight to the DSCR page. If it is missing or below 1.25, I close the file. I do not look at anything else. I do not have time to check 50 files a day. DSCR below 1.25 = reject.”

EMI Repayment Schedule (First 12 Months):

| Month | Opening Balance (₹) | EMI (₹) | Interest (₹) | Principal (₹) | Closing Balance (₹) |

|---|---|---|---|---|---|

| 1 | 1,90,000 | 4,000 | 1,702 | 2,298 | 1,87,702 |

| 2 | 1,87,702 | 4,000 | 1,681 | 2,319 | 1,85,383 |

| 3 | 1,85,383 | 4,000 | 1,661 | 2,339 | 1,83,044 |

| 4 | 1,83,044 | 4,000 | 1,640 | 2,360 | 1,80,684 |

| 5 | 1,80,684 | 4,000 | 1,619 | 2,381 | 1,78,303 |

| 6 | 1,78,303 | 4,000 | 1,598 | 2,402 | 1,75,901 |

| 7 | 1,75,901 | 4,000 | 1,577 | 2,423 | 1,73,478 |

| 8 | 1,73,478 | 4,000 | 1,555 | 2,445 | 1,71,033 |

| 9 | 1,71,033 | 4,000 | 1,533 | 2,467 | 1,68,566 |

| 10 | 1,68,566 | 4,000 | 1,511 | 2,489 | 1,66,077 |

| 11 | 1,66,077 | 4,000 | 1,488 | 2,512 | 1,63,565 |

| 12 | 1,63,565 | 4,000 | 1,466 | 2,534 | 1,61,031 |

📌 WHY THIS MATTERS: This table shows the bank that you can repay the loan. Month by month. Your closing balance goes down every month. That is what they want to see.

Ready for the next step? Keep reading.

CHAPTER 5: COMPLETE SAMPLE PROJECT REPORT (EXISTING BUSINESS – KIRANA STORE)

Here is a complete sample project report for an existing kirana store. Use this as a reference.

Business Name: Ramesh Kirana Store

Owner: Ramesh Kumar Gupta

Location: Mani Majra, Chandigarh

Loan Amount: ₹2,00,000

Loan Type: Kishore (Mudra Loan)

Executive Summary:

| Field | Value |

|---|---|

| Business Name | Ramesh Kirana Store |

| Owner Name | Ramesh Kumar Gupta |

| Loan Amount | ₹2,00,000 |

| Loan Purpose | Working capital and stock purchase |

| Annual Revenue | ₹9,60,000 |

| Net Profit (Year 1) | ₹68,575 |

| DSCR | 2.00 |

| Tenure | 5 Years |

Project Cost & Means of Finance:

| Particulars | Amount (₹) |

|---|---|

| Fixed Assets | 70,000 |

| Initial Stock | 1,20,000 |

| Working Capital | 10,000 |

| Total | 2,00,000 |

| Source | Amount (₹) | % |

|---|---|---|

| Own Contribution | 10,000 | 5% |

| Bank Loan | 1,90,000 | 95% |

5-Year P&L:

| Year | Sales (₹) | Gross Profit (₹) | Net Profit (₹) | DSCR |

|---|---|---|---|---|

| 1 | 9,60,000 | 2,40,000 | 68,575 | 2.00 |

| 2 | 10,56,000 | 2,64,000 | 89,037 | 2.35 |

| 3 | 11,40,480 | 2,85,120 | 1,07,020 | 2.63 |

| 4 | 12,08,909 | 3,02,227 | 1,21,221 | 2.82 |

| 5 | 12,58,589 | 3,14,647 | 1,30,881 | 2.91 |

This report was approved by SBI Mani Majra branch in 12 days.

CHAPTER 6: COMPLETE SAMPLE PROJECT REPORT (NEW BUSINESS – BEAUTY PARLOUR)

Here is a complete sample project report for a new beauty parlour. New businesses are different. You do not have past sales data. So you focus on your establishment plan instead.

Business Name: Priya Beauty Parlour

Owner: Priya Sharma

Location: Indira Nagar, Lucknow

Loan Amount: ₹1,50,000

Loan Type: Kishore (Mudra Loan)

Executive Summary:

| Field | Value |

|---|---|

| Business Name | Priya Beauty Parlour |

| Owner Name | Priya Sharma |

| Loan Amount | ₹1,50,000 |

| Loan Purpose | Interior setup and equipment purchase |

| Annual Revenue (Projected) | ₹6,00,000 |

| Net Profit (Projected Year 1) | ₹65,000 |

| DSCR (Projected) | 1.85 |

| Tenure | 5 Years |

Establishment Plan (Instead of Past Performance):

| Activity | Timeline |

|---|---|

| Shop rental agreement | Month 1, Week 1 |

| Interior work | Month 1, Week 2-3 |

| Equipment purchase | Month 1, Week 4 |

| Staff hiring (1 assistant) | Month 2, Week 1 |

| Grand opening | Month 2, Week 2 |

Project Cost & Means of Finance:

| Particulars | Amount (₹) |

|---|---|

| Interior (painting, flooring, mirrors) | 50,000 |

| Equipment (chairs, hair dryer, steamer) | 60,000 |

| Beauty products (initial stock) | 30,000 |

| Marketing (first month) | 10,000 |

| Total | 1,50,000 |

| Source | Amount (₹) | % |

|---|---|---|

| Own Contribution | 15,000 | 10% |

| Bank Loan | 1,35,000 | 90% |

5-Year P&L (Projected):

| Year | Sales (₹) | Gross Profit (₹) | Net Profit (₹) | DSCR |

|---|---|---|---|---|

| 1 | 6,00,000 | 2,10,000 | 65,000 | 1.85 |

| 2 | 7,20,000 | 2,52,000 | 85,000 | 2.10 |

| 3 | 8,40,000 | 2,94,000 | 1,05,000 | 2.35 |

| 4 | 9,60,000 | 3,36,000 | 1,25,000 | 2.60 |

| 5 | 10,80,000 | 3,78,000 | 1,45,000 | 2.85 |

Note for new businesses: Your Year 1 sales will be lower than existing businesses. That is normal. Banks understand this. What matters is that you show growth over time.

CHAPTER 7: HOW TO MAKE A PROJECT REPORT USING MUDRAREADY – 6 SIMPLE STEPS

You now know the 7 steps to make a project report manually.

But there is an easier way.

You do not need to understand DSCR. You do not need to understand MPBF. You do not need to build complex financial models in Excel.

MudraReady asks you 12 simple questions. Then it automatically generates a complete 20-27 page project report with all the calculations.

Here is how it works.

Step 1: Visit MudraReady and Click “Report Banayein”

Go to mudraready.in. Click the button that says “Report Banayein” or “Get Your Report”.

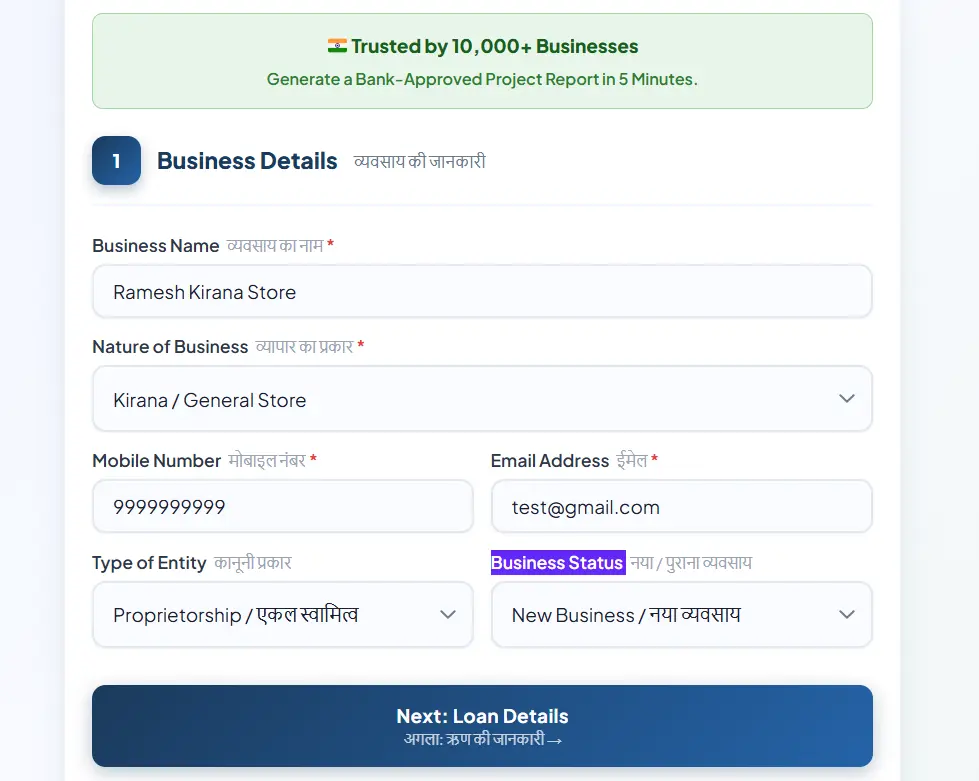

Step 2: Enter Your Business Details (6 Questions)

| Question | What to Enter | Example |

|---|---|---|

| Business Name | Your shop/business name | “Ramesh Kirana Store” |

| Nature of Business | Select from 30+ options | “Kirana / General Store” |

| Mobile Number | Your 10-digit number | “999999999” |

| Email Address | Your email | “test@gmail.com” |

| Type of Entity | Business Type | Proprietorship |

| Business Status | New Or Old | New |

⚠️ IMPORTANT: Select “New Business” if you are starting from zero. Select “Existing Business” if you already have a running shop. The report format changes automatically based on your selection.

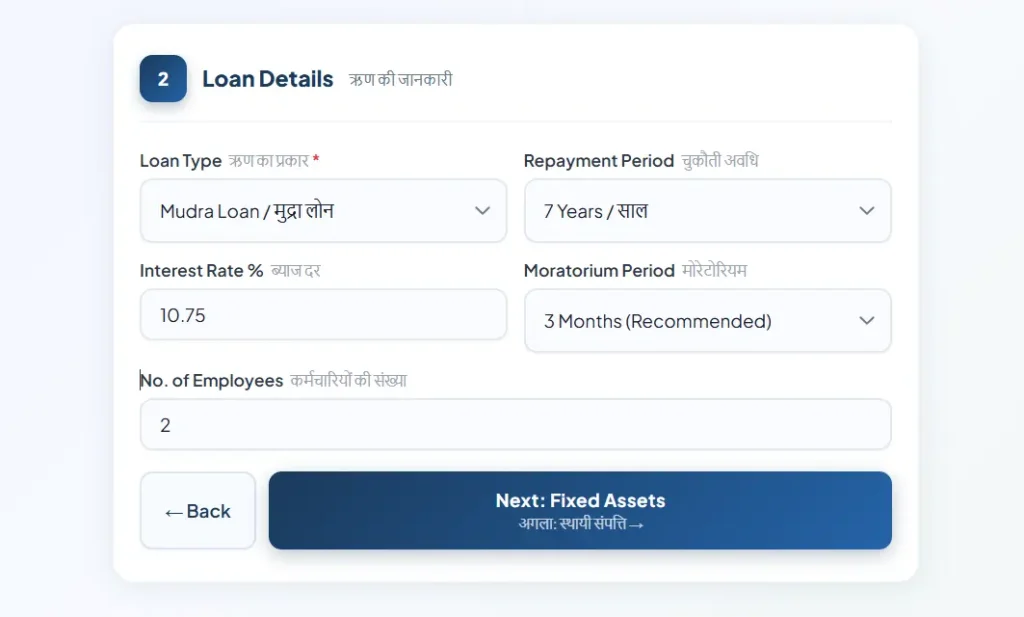

Step 3: Enter Loan Details (3 Questions)

| Question | What to Enter | Example |

|---|---|---|

| Loan Type | Mudra / PMEGP / MSME | “Mudra Loan” |

| Loan Amount | How much you need (₹50,000 to ₹10,00,000) | “2,00,000” |

| Repayment Period | 3, 5, or 7 years | “5 years” |

Step 4: Enter Asset Details (2 Questions)

| Question | What to Enter | Example |

|---|---|---|

| Fixed Assets | Machinery, furniture, vehicle, interior cost | “70,000” |

| Working Capital Required | Day-to-day cash needed for stock and expenses | “1,30,000” |

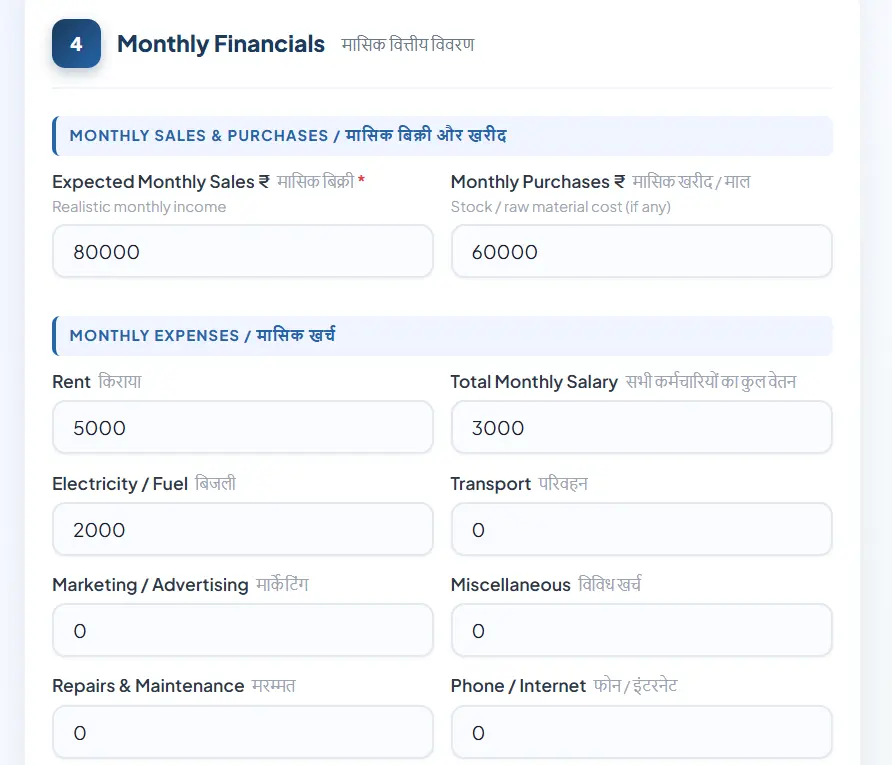

Step 5: Enter Monthly Financials (6 Questions)

| Question | What to Enter | Example |

|---|---|---|

| Monthly Revenue / Sales | Your average monthly sales | “80,000” |

| Monthly Purchases | Cost of goods sold per month | “60,000” |

| Monthly Rent | Shop rent | “5,000” |

| Monthly Salary (Total) | Total wages for all staff | “3,000” |

| Monthly Electricity | Power bill | “2,000” |

| Other Monthly Expenses | Transport, marketing, misc. | “2,000” |

Step 6: Enter Promoter Details (3 Questions)

| Question | What to Enter | Example |

|---|---|---|

| Owner Full Name | Exactly as per Aadhaar | “Ramesh Kumar Gupta” |

| Father’s Name | Father’s full name | “Rajesh Kumar Gupta” |

| Education & Experience | Your background | “12th Pass, 5 years experience” |

That is it. 12 questions. 5-7 minutes.

After you submit, the system automatically: See Sample Project Report

| Calculation | What It Produces |

|---|---|

| DSCR (Debt Service Coverage Ratio) | Year-by-year for 5 years |

| MPBF (Working Capital Calculation) | Tandon Committee Method 1 |

| Profit & Loss Statement | 5 year projection |

| Balance Sheet | 5 year projection |

| Cash Flow Statement | 5 year projection |

| EMI Repayment Schedule | Month-by-month for full tenure |

| Break-even Analysis | Sales needed to cover costs |

| Depreciation Schedule | Year-by-year |

| Sensitivity Analysis | What if sales drop 5% or 10% |

You get your bank-ready project report in 30 minutes. ₹399 only.

👉 [Make your project report here – 30 minutes, ₹399 only]

CHAPTER 8: 7 COMMON MISTAKES THAT RUIN YOUR PROJECT REPORT (WITH REAL REJECTION STORIES)

Mistake #1: Overestimating Sales

A bakery owner in Agra projected ₹50 lakh profit in Year 1. His shop was 200 sq. ft. His area had 3 other bakeries.

The bank rejected his application. The loan officer told him: “Even big bakeries in Delhi do not make ₹50 lakh in Year 1. Be realistic.”

The fix: Use industry averages. 10-20% year-on-year growth is realistic. 200% is not.

Mistake #2: No Own Contribution (0% Margin Money)

A tailor in Patna asked for a ₹3 lakh loan. He had saved nothing. He wanted the bank to pay 100%.

The bank rejected him. The loan officer said: “If you have not saved anything, why should we trust you with our money?”

The fix: Save 5-10% of the project cost before applying. Show bank statement as proof.

Mistake #3: Vague Loan Purpose

A mobile repair shop owner wrote: “I need money for my business.” That is it. No details.

The bank rejected him. The loan officer said: “We do not know where our money is going.”

The fix: Be specific. “I need ₹2 lakh for a new stitching machine and raw material” works. “I need money for business” does not.

Mistake #4: No DSCR Calculation

A beauty parlour owner submitted a 5-page project report. It had no DSCR section.

The bank rejected her. The loan officer said: “How do we know you can pay the EMI?”

The fix: Include DSCR in your project report. Keep it above 1.25.

Mistake #5: Name Mismatch Across Documents

A dairy farmer’s Aadhaar said “Gurmeet Singh”. His PAN said “Gurmeet S”. His application said “Gurmeet Singh Brar”.

The bank rejected him. The loan officer said: “We cannot verify your identity.”

The fix: Ensure EXACT same name on Aadhaar, PAN, and application form.

Mistake #6: Missing Udyam Registration

A hardware store owner applied for a ₹4 lakh Kishore loan. He did not have Udyam Registration.

The bank rejected him. The loan officer said: “Udyam is mandatory for Kishore loans now.”

The fix: Register for FREE at udyamregistration.gov.in. Takes 5 minutes.

Mistake #7: Submitting Old Bank Statement

A restaurant owner submitted a bank statement from 8 months ago.

The bank rejected him. The loan officer said: “We need current financial position. Not 8 months old.”

The fix: Download fresh bank statement within 30 days of applying.

CHAPTER 9: WHAT TO DO AFTER MAKING YOUR PROJECT REPORT

Your project report is ready. Now what?

| Step | Action | Time Required |

|---|---|---|

| 1 | Get Udyam Registration (FREE) | 5 minutes |

| 2 | Collect all supporting documents | 1-2 hours |

| 3 | Print 2 copies of your project report | 10 minutes |

| 4 | Visit your bank branch | 2-4 hours |

| 5 | Submit application and get reference number | 30 minutes |

| 6 | Follow up every 3-4 days | 5 minutes each time |

Supporting Documents Checklist:

| Document | Status |

|---|---|

| Aadhaar Card (original + copy) | ☐ |

| PAN Card | ☐ |

| Udyam Registration Certificate | ☐ |

| Shop & Establishment License | ☐ |

| Bank Statement (last 12 months) | ☐ |

| ITR (if loan above ₹2 lakh) | ☐ |

| 2 Passport Size Photographs | ☐ |

| Project Report (printed) | ☐ |

| Quotations (if buying assets) | ☐ |

👉 [Need the full document checklist? Read our complete guide]

CHAPTER 10: FREQUENTLY ASKED QUESTIONS (12 QUESTIONS)

Q1. Do I need a CA to make a project report for Mudra loan?

No. You do not need a CA. The official Mudra loan application does not require a CA signature. Many banks accept self-made or automated project reports. However, some banks may ask for CA certification for loans above ₹2 lakh. MudraReady offers a CA Assistance add-on (₹799 extra) if your bank requires it.

Q2. Can I make a project report myself without any experience?

Yes. You can use the 7 steps in this guide to make a project report manually. Or you can use MudraReady which asks 12 simple questions and generates the report automatically. No financial experience required.

Q3. Is project report mandatory for all Mudra loans?

No. Shishu loans (up to ₹50,000) do not require a project report. Kishore, Tarun, and Tarun Plus loans require a project report.

Q4. What is DSCR? Can you explain in simple words?

DSCR tells the bank whether your business earns enough profit to pay the EMI. If your DSCR is 2.00, for every ₹1 of EMI you need to pay, your business earns ₹2. Banks want DSCR above 1.25.

Q5. How much does a project report cost from a CA?

A CA typically charges between ₹2,000 and ₹10,000 for a Mudra loan project report. The price depends on your loan amount and location. MudraReady charges ₹399 for the same report.

Q6. How long does it take to make a project report?

A CA takes 3 to 5 days. Making it yourself using the 7 steps takes 2-3 days. Using MudraReady takes 30 minutes.

Q7. What is the minimum DSCR required for Mudra loan?

The bank requires DSCR above 1.25. If your DSCR is below 1.25, your application will be rejected.

Q8. Can I use the same project report for different banks?

Yes. The format is standard across all public sector banks (SBI, PNB, Bank of Baroda, IOB, Canara Bank, etc.). Private banks like HDFC and ICICI may have slightly different requirements.

Q9. What is the difference between Shishu, Kishore, and Tarun project reports?

Shishu: No project report needed. Kishore: 20-25 page report with basic financial projections. Tarun: 25-30 page report with detailed financials, DSCR, MPBF, and sensitivity analysis.

Q10. Where can I get a project report sample for free?

You can download a free sample project report from MudraReady. The sample has watermark on financial data, but shows you the complete format.

Q11. Can I apply for a Mudra loan if I am starting a new business?

Yes. Mudra loans are for both new and existing businesses. For new businesses, your project report needs an “Establishment Plan” instead of “Past Performance”. MudraReady has a “New Business” option – select it when filling the form, and the report will be formatted correctly.

Q12. My DSCR is below 1.25. What should I do?

Increase your sales projection, reduce your expense projection, reduce your loan amount, or increase your loan tenure. Any of these actions will improve your DSCR. Do not submit a report with DSCR below 1.25 – the bank will reject it automatically.

👉 [Download free sample project report]

CHAPTER 11: CONCLUSION – YOUR LOAN APPROVAL STARTS HERE

You now know exactly how to make a project report for Mudra loan.

Let us recap what you learned.

| What You Learned | Key Takeaway |

|---|---|

| What is a project report | A 20-27 page document that tells the bank about your business and loan |

| 7 steps to make a report | Executive summary, business profile, market analysis, operations, cost, finances, DSCR |

| Sample report (existing business) | Ramesh Kirana Store – approved by SBI in 12 days |

| Sample report (new business) | Priya Beauty Parlour – projected approval |

| Common mistakes | Overestimating sales, no margin money, vague descriptions, no DSCR |

| MudraReady 6-step process | 12 questions, 30 minutes, ₹399 |

| What to do after | Get Udyam, collect documents, apply, follow up |

You have two options now.

Option 1: Make the project report yourself using the 7 steps in this guide. It will take 2-3 days. You will need to learn DSCR, MPBF, financial projections, and balance sheets.

Option 2: Use MudraReady. Answer 12 simple questions. Get your bank-ready project report in 30 minutes. ₹399 only.

Both options work. Both options give you a report that banks accept.

The choice is yours.

But remember: Every day you wait to apply for your Mudra loan:

- Your competitor buys that stock you wanted

- Your customer goes to someone else

- Your shop stays smaller than it should be

- Your family waits longer for a better life

Stop waiting.

👉 Make your bank-ready project report here – 30 minutes, ₹399 only

ABOUT THE AUTHOR

This guide was created by the MudraReady team.

We have done what most CAs have not:

- Visited 15+ bank branches across Uttar Pradesh, Bihar, and Punjab

- Sat across from loan officers at SBI, PNB, and Bank of Baroda

- Asked them directly: “What makes you approve a project report?”

- Analyzed 50+ rejected applications to find the real reasons

We took their answers and built a system.

A system that asks you 12 simple questions. And gives you a bank-ready project report in 30 minutes.

No CA. No ₹5,000. No 5-day wait.

Just your loan approval, faster.

Have questions? WhatsApp us at 7888513976. We reply within 30 minutes.

RELATED GUIDES

- Mudra Loan Documents List 2026 – Complete Checklist

- Why Banks Reject Mudra Loans – 7 Reasons and How to Fix Them

- DSCR Calculation for Mudra Loan – Simple Formula with Example

- Project Report for Kirana Store – Complete Guide

Last updated: May 2026

Sources: Mudra Bank official guidelines, State Bank of India MSME document checklist, Punjab National Bank project report requirements, multiple branch manager interviews across UP, Bihar, and Punjab.