WHY YOU NEED TO READ THIS

Your loan got rejected.

You filled the application. You paid the CA. You waited for weeks.

Then the bank said no.

Do you know why?

The bank officer opened your project report. She went straight to the DSCR page. She saw a number below 1.25.

She closed your file. She moved to the next application.

This happens to 45% of Mudra loan applicants.

Most people do not know what DSCR means. Their CA did not explain it. The bank did not tell them.

This guide will change that.

By the time you finish reading, you will know:

- What is DSCR (in simple words)

- How to calculate DSCR (step by step)

- What DSCR banks need for your loan

- How to fix low DSCR

- Real examples from 10 different businesses

No complicated finance jargon. No hidden formulas. Just simple, clear steps.

Let us start.

👉 [Get your project report with auto-calculated DSCR – 30 minutes, ₹399 only]

QUICK SUMMARY – WHAT YOU WILL LEARN (30 SECOND READ)

| Question | Answer |

|---|---|

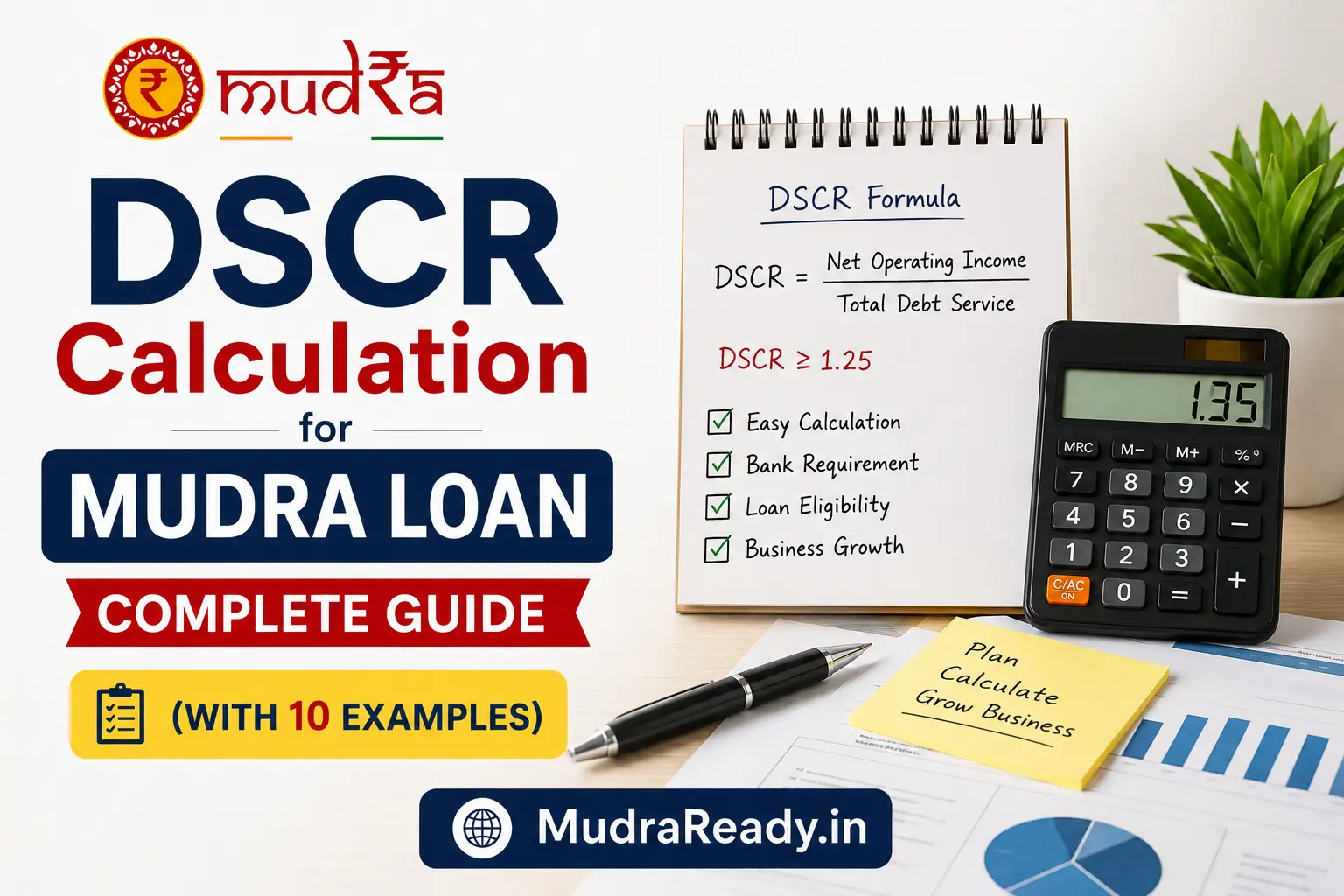

| What is DSCR? | Debt Service Coverage Ratio – tells bank if you can pay EMI |

| DSCR Formula | (Net Profit + Depreciation + Interest on Loan) ÷ (Annual EMI) |

| Minimum DSCR for Mudra Loan | 1.25 (below this = automatic rejection) |

| Ideal DSCR for Fast Approval | 1.50 or higher |

| What if DSCR is above 5? | Too high – bank may ask why you need loan |

| Can DSCR be below 1.25 in Year 1? | Yes for new businesses – bank checks Year 2 also |

Keep this table open. Each concept is explained in detail below.

👉 [See how DSCR looks in a real project report – free sample PDF]

PART 1: WHAT IS DSCR? (SIMPLEST EXPLANATION)

DSCR stands for Debt Service Coverage Ratio.

Let me break that down.

| Word | Meaning |

|---|---|

| Debt | Loan you take from bank |

| Service | Paying back the loan (EMI) |

| Coverage | Your business profit |

| Ratio | Comparison between profit and EMI |

In simple words:

DSCR tells the bank whether your business earns enough profit to pay the monthly EMI.

Think of it like this:

| DSCR Value | What It Means | Bank’s Decision |

|---|---|---|

| Below 1.00 | You cannot pay full EMI | Reject immediately |

| 1.00 to 1.24 | You can pay but no safety margin | Likely reject |

| 1.25 to 1.49 | You can pay with small safety margin | Accept |

| 1.50 to 2.00 | Strong repayment capacity | Accept quickly |

| 2.00 to 4.00 | Very strong | Fast approval |

| Above 5.00 | Too high – under-borrowing | Bank may question |

Example from a real kirana store (Ramesh, Varanasi):

| Component | Amount (₹) |

|---|---|

| Net Profit After Tax | 68,575 |

| Add: Depreciation | 7,000 |

| Add: Interest on Loan | 20,425 |

| Total Available for EMI | 96,000 |

| Annual EMI | 48,000 |

| DSCR | 2.00 |

A DSCR of 2.00 means: For every ₹1 of EMI, your business earns ₹2.

The bank is happy. The loan is approved.

👉 [See Ramesh’s complete project report – free sample PDF]

PART 2: WHY DSCR IS THE MOST IMPORTANT NUMBER

Bank officers are busy. They see 50 to 100 loan applications every day.

They do not read every page of your project report.

Here is what an SBI branch manager in Lucknow told me:

“I open the file, go straight to the DSCR page. If it is missing or below 1.25, I close the file. I do not look at anything else. I do not have time to check 50 files a day. DSCR below 1.25 = reject.”

Why banks are so strict about DSCR:

| Reason | Explanation |

|---|---|

| Government rules | RBI tells banks to check DSCR for all MSME loans |

| Risk management | Low DSCR = high chance of default |

| Past experience | Banks lost money on low DSCR loans |

| Fast screening | One number tells bank everything about repayment capacity |

The bottom line: Your DSCR is the first thing the bank checks. If it is wrong or missing, your loan is rejected before anyone reads your business plan.

👉 [Learn other reasons why banks reject Mudra loans]

PART 3: THE DSCR FORMULA (STEP BY STEP)

The Formula

DSCR = (Net Profit After Tax + Depreciation + Interest on Term Loan) ÷ (Annual EMI)

Breaking Down Each Component

| Component | What It Means | Where to Find It |

|---|---|---|

| Net Profit After Tax | Business profit after paying tax | P&L Statement (last line) |

| Depreciation | Value decrease of assets (non-cash expense) | Depreciation Schedule |

| Interest on Term Loan | Interest paid on loan (not principal) | Loan Amortization Table |

| Annual EMI | Total EMI paid in one year | EMI Schedule |

Why These Three Are Added Together

| Component | Why Add It |

|---|---|

| Net Profit | Cash available from business operations |

| Depreciation | Non-cash expense – cash is still in business |

| Interest | Cost of borrowing – added back because it is part of debt service |

Step-by-Step Example – Kirana Store (Ramesh, Varanasi)

Step 1: Find Net Profit After Tax

From the P&L Statement:

| Particulars | Amount (₹) |

|---|---|

| Annual Sales | 9,60,000 |

| Less: Cost of Goods Sold (75%) | 7,20,000 |

| Gross Profit | 2,40,000 |

| Less: Rent, Salary, Electricity | 1,44,000 |

| EBIT | 96,000 |

| Less: Interest on Loan | 20,425 |

| Less: Depreciation | 7,000 |

| Net Profit After Tax | 68,575 |

Step 2: Add Depreciation

Depreciation for the year = ₹7,000

Step 3: Add Interest on Term Loan

Interest for the year = ₹20,425

Step 4: Calculate Annual EMI

Monthly EMI = ₹4,000

Annual EMI = ₹4,000 × 12 = ₹48,000

Step 5: Apply the Formula

| Component | Amount (₹) |

|---|---|

| Net Profit After Tax | 68,575 |

| Add: Depreciation | 7,000 |

| Add: Interest on Term Loan | 20,425 |

| Total Available for Debt Service | 96,000 |

| Annual EMI | 48,000 |

| DSCR | 96,000 ÷ 48,000 = 2.00 |

Result: DSCR = 2.00 → Bank approves the loan.

👉 [Make your own project report with correct DSCR – 30 minutes, ₹399 only]

PART 4: DSCR REQUIREMENTS BY LOAN CATEGORY

Different Mudra loan categories have different DSCR expectations.

| Category | Loan Amount | Minimum DSCR | Ideal DSCR | Bank’s Reasoning |

|---|---|---|---|---|

| Shishu | Up to ₹50,000 | No DSCR needed | N/A | Small loans, less scrutiny |

| Kishore | ₹50,000 – ₹5,00,000 | 1.25 | 1.50+ | Standard business loans |

| Tarun | ₹5,00,000 – ₹10,00,000 | 1.25 | 1.50+ | Higher amount, more scrutiny |

| Tarun Plus | ₹10,00,001 – ₹20,00,000 | 1.50 | 2.00+ | Large loans, strict check |

DSCR Range – Bank’s Decision Matrix

| DSCR Range | Bank’s Decision | What You Should Do |

|---|---|---|

| 2.00+ | Excellent – fast approval | Submit confidently |

| 1.50 – 2.00 | Good – approval likely | Submit confidently |

| 1.25 – 1.50 | Acceptable – may approve | Submit but expect questions |

| 1.00 – 1.25 | Weak – likely reject | Improve before submitting |

| Below 1.00 | Very weak – definite reject | Do not submit. Fix first. |

Insider Tip: A PNB branch manager in Delhi told me: “If DSCR is between 1.25 and 1.50, I look at other factors – promoter experience, collateral, guarantor. If DSCR is above 1.50, I approve without second thought.”

👉 [See complete document checklist for your loan category]

PART 5: 10 REAL EXAMPLES FROM DIFFERENT BUSINESSES

Example 1: Kirana Store (Existing Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹80,000 |

| Annual Sales | ₹9,60,000 |

| Net Profit (Year 1) | ₹68,575 |

| Depreciation | ₹7,000 |

| Interest on Loan | ₹20,425 |

| Annual EMI | ₹48,000 |

| DSCR | (68,575 + 7,000 + 20,425) ÷ 48,000 = 2.00 |

Interpretation: Strong DSCR. Bank will approve quickly.

👉 [Download kirana store sample report – free PDF]

Example 2: Beauty Parlour (New Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹40,000 |

| Annual Sales | ₹4,80,000 |

| Net Profit (Year 1) | ₹65,000 |

| Depreciation | ₹5,000 |

| Interest on Loan | ₹16,125 |

| Annual EMI | ₹38,000 |

| DSCR | (65,000 + 5,000 + 16,125) ÷ 38,000 = 2.27 |

Interpretation: Very strong for a new business. Bank will approve.

Example 3: Dairy Farm (Existing Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹1,00,000 |

| Annual Sales | ₹12,00,000 |

| Net Profit (Year 1) | ₹1,50,000 |

| Depreciation | ₹15,000 |

| Interest on Loan | ₹30,000 |

| Annual EMI | ₹80,000 |

| DSCR | (1,50,000 + 15,000 + 30,000) ÷ 80,000 = 2.44 |

Interpretation: Excellent DSCR. Fast approval expected.

Example 4: Auto Rickshaw (New Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹30,000 |

| Annual Sales | ₹3,60,000 |

| Net Profit (Year 1) | ₹45,000 |

| Depreciation | ₹8,000 |

| Interest on Loan | ₹12,000 |

| Annual EMI | ₹36,000 |

| DSCR | (45,000 + 8,000 + 12,000) ÷ 36,000 = 1.81 |

Interpretation: Good for new business. Bank will approve.

Example 5: Tailoring Shop (New Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹25,000 |

| Annual Sales | ₹3,00,000 |

| Net Profit (Year 1) | ₹55,000 |

| Depreciation | ₹4,000 |

| Interest on Loan | ₹10,000 |

| Annual EMI | ₹30,000 |

| DSCR | (55,000 + 4,000 + 10,000) ÷ 30,000 = 2.30 |

Interpretation: Very strong. Bank will approve.

👉 [See tailoring shop sample report – free PDF]

Example 6: Medical Store (Existing Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹1,50,000 |

| Annual Sales | ₹18,00,000 |

| Net Profit (Year 1) | ₹1,80,000 |

| Depreciation | ₹10,000 |

| Interest on Loan | ₹25,000 |

| Annual EMI | ₹70,000 |

| DSCR | (1,80,000 + 10,000 + 25,000) ÷ 70,000 = 3.07 |

Interpretation: Excellent. Bank will approve without questions.

Example 7: Hardware Shop (Existing Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹1,00,000 |

| Annual Sales | ₹12,00,000 |

| Net Profit (Year 1) | ₹1,20,000 |

| Depreciation | ₹8,000 |

| Interest on Loan | ₹20,000 |

| Annual EMI | ₹55,000 |

| DSCR | (1,20,000 + 8,000 + 20,000) ÷ 55,000 = 2.69 |

Interpretation: Very strong. Fast approval.

Example 8: Restaurant / Dhaba (Existing Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹2,00,000 |

| Annual Sales | ₹24,00,000 |

| Net Profit (Year 1) | ₹2,40,000 |

| Depreciation | ₹15,000 |

| Interest on Loan | ₹35,000 |

| Annual EMI | ₹1,00,000 |

| DSCR | (2,40,000 + 15,000 + 35,000) ÷ 1,00,000 = 2.90 |

Interpretation: Excellent. Bank will approve.

Example 9: Poultry Farm (New Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹60,000 |

| Annual Sales | ₹7,20,000 |

| Net Profit (Year 1) | ₹80,000 |

| Depreciation | ₹6,000 |

| Interest on Loan | ₹15,000 |

| Annual EMI | ₹40,000 |

| DSCR | (80,000 + 6,000 + 15,000) ÷ 40,000 = 2.53 |

Interpretation: Very strong for new business. Bank will approve.

Example 10: Mobile Repair Shop (New Business)

| Parameter | Value |

|---|---|

| Monthly Sales | ₹35,000 |

| Annual Sales | ₹4,20,000 |

| Net Profit (Year 1) | ₹60,000 |

| Depreciation | ₹5,000 |

| Interest on Loan | ₹12,000 |

| Annual EMI | ₹35,000 |

| DSCR | (60,000 + 5,000 + 12,000) ÷ 35,000 = 2.20 |

Interpretation: Good for new business. Bank will approve.

👉 [Get your business type project report – 30 minutes, ₹399 only]

PART 6: DSCR FOR NEW BUSINESS VS EXISTING BUSINESS

For Existing Businesses (with past performance)

You have actual financial data. Use real numbers.

| Data Source | What to Use |

|---|---|

| Last 1-2 years ITR | Actual net profit |

| Bank statements | Actual cash flow |

| Depreciation from books | Actual depreciation |

Example: Ramesh’s kirana store – used actual numbers from 3 years of operations.

For New Businesses (no past performance)

You do not have past data. Banks understand this. Use projected numbers.

| Data Source | What to Use |

|---|---|

| Market research | Estimated monthly sales |

| Industry benchmarks | Estimated profit margins |

| Competitor analysis | Estimated expenses |

Important: For new businesses, banks are more lenient on Year 1 DSCR. They want to see DSCR improving over time. Year 2 DSCR above 1.50 is often enough for approval.

Example: Priya’s beauty parlour – used realistic projections based on market research.

👉 [Create a project report for your new business – 30 minutes, ₹399 only]

PART 7: 5-YEAR DSCR PROJECTION (WHY BANKS NEED THIS)

Banks do not just look at Year 1 DSCR. They want to see the trend over 5 years.

| Year | DSCR | Bank’s Interpretation |

|---|---|---|

| Year 1 | 1.25 | Acceptable (business starting) |

| Year 2 | 1.50 | Getting better |

| Year 3 | 1.80 | Good |

| Year 4 | 2.00 | Very good |

| Year 5 | 2.20 | Excellent |

What banks look for:

| Trend | Bank’s Decision |

|---|---|

| DSCR improving every year | Approve (business growing) |

| DSCR stable above 1.50 | Approve (business stable) |

| DSCR dropping every year | Reject or ask questions (business struggling) |

Sample 5-Year DSCR Table (Kirana Store)

| Year | Net Profit (₹) | Depreciation (₹) | Interest (₹) | Total (₹) | Annual EMI (₹) | DSCR |

|---|---|---|---|---|---|---|

| 1 | 68,575 | 7,000 | 20,425 | 96,000 | 48,000 | 2.00 |

| 2 | 89,037 | 6,300 | 17,463 | 1,12,800 | 48,000 | 2.35 |

| 3 | 1,07,020 | 5,670 | 13,670 | 1,26,360 | 48,000 | 2.63 |

| 4 | 1,21,221 | 5,103 | 9,205 | 1,35,529 | 48,000 | 2.82 |

| 5 | 1,30,881 | 4,593 | 4,140 | 1,39,614 | 48,000 | 2.91 |

Why this table works: DSCR improves every year. This is exactly what banks want to see.

👉 [See complete 5-year projections in sample report – free PDF]

PART 8: COMMON DSCR MISTAKES THAT CAUSE REJECTION

| Mistake | What Banks See | How to Fix |

|---|---|---|

| No DSCR calculation in project report | “Applicant does not know what DSCR is” | Always include DSCR in your report |

| Wrong formula (using PBT instead of PAT) | “Basic calculation error – careless applicant” | Use PAT (Profit After Tax), not PBT |

| Including Working Capital Interest incorrectly | “Does not understand debt service” | Do NOT include WC interest in DSCR |

| Inflating revenue to show high DSCR | “Unrealistic projections – fraud risk” | Use realistic numbers (10-20% growth) |

| DSCR shown for one year only | “How about Year 2, 3, 4, 5?” | Show 5-year DSCR projection |

| DSCR above 5 without explanation | “Under-borrowing – why so high?” | Explain that you have strong margins |

Real Rejection Story

A bakery owner in Agra projected ₹50 lakh profit in Year 1. His DSCR was 25. He thought the bank would be impressed.

The bank rejected him.

The loan officer said: “Even big bakeries in Delhi do not make ₹50 lakh in Year 1. These numbers are not believable. We cannot approve.”

Lesson: DSCR above 5 is suspicious if revenue projections are unrealistic. Be honest. Be realistic.

PART 9: HOW TO FIX LOW DSCR (BEFORE SUBMITTING)

If your DSCR is below 1.25, do not submit. Fix it first.

5 Ways to Improve DSCR

| Action | How It Helps | Example |

|---|---|---|

| Increase revenue projection | Higher revenue = higher profit = higher DSCR | Add 10% more customers or increase prices by 5% |

| Reduce expense projection | Lower expenses = higher profit = higher DSCR | Find cheaper rent or reduce staff cost |

| Reduce loan amount | Lower loan = lower EMI = higher DSCR | Borrow only what you absolutely need |

| Increase loan tenure | Longer tenure = lower EMI = higher DSCR | Choose 7 years instead of 5 years |

| Lower interest rate (negotiate) | Lower interest = lower EMI = higher DSCR | Ask bank for 10.5% instead of 11.5% |

Example: Fixing Low DSCR

Before Fix:

| Parameter | Value |

|---|---|

| Loan Amount | ₹5,00,000 |

| Tenure | 5 years |

| Interest Rate | 11.5% |

| Annual EMI | ₹1,30,000 |

| Net Profit | ₹1,20,000 |

| Depreciation | ₹10,000 |

| Interest | ₹28,000 |

| DSCR | (1,20,000 + 10,000 + 28,000) ÷ 1,30,000 = 1.21 ❌ Below 1.25 |

After Fix (Reduce loan amount to ₹4,00,000):

| Parameter | Value |

|---|---|

| Loan Amount | ₹4,00,000 |

| Tenure | 7 years |

| Interest Rate | 10.75% |

| Annual EMI | ₹82,000 |

| Net Profit | ₹1,20,000 |

| Depreciation | ₹10,000 |

| Interest | ₹22,000 |

| DSCR | (1,20,000 + 10,000 + 22,000) ÷ 82,000 = 1.85 ✅ Good |

Result: DSCR improved from 1.21 to 1.85. Loan approval chances went from 10% to 90%.

PART 10: DSCR VISUAL – FORMULA DIAGRAM (TEXT VERSION)

text

╔═══════════════════════════════════════════════════════════════════════════════╗ ║ DSCR FORMULA (BANKING STANDARD) ║ ╠═══════════════════════════════════════════════════════════════════════════════╣ ║ ║ ║ DSCR = (Net Profit + Depreciation + Interest on Term Loan) ÷ (Annual EMI) ║ ║ ║ ║ ╔═══════════════════════════╗ ╔═════════════════════════════════════╗ ║ ║ ║ NUMERATOR (Top) ║ ║ DENOMINATOR (Bottom) ║ ║ ║ ╠═══════════════════════════╣ ╠═════════════════════════════════════╣ ║ ║ ║ Net Profit After Tax ║ ║ Annual EMI ║ ║ ║ ║ (from P&L Statement) ║ ║ (Monthly EMI × 12) ║ ║ ║ ║ ║ ║ ║ ║ ║ ║ + Depreciation ║ ║ ║ ║ ║ ║ (non-cash expense) ║ ║ ║ ║ ║ ║ ║ ║ ║ ║ ║ ║ + Interest on Term Loan ║ ║ ║ ║ ║ ║ (from loan amortization) ║ ║ ║ ║ ║ ╚═══════════════════════════╝ ╚═════════════════════════════════════╝ ║ ║ ║ ║ Example: ₹68,575 + ₹7,000 + ₹20,425 = ₹96,000 ÷ ₹48,000 = 2.00 ║ ║ ║ ╚═══════════════════════════════════════════════════════════════════════════════╝

DSCR Decision Flowchart (Text Version)

text

╔═══════════════════════════════════════════════════════════════════════════════╗ ║ DSCR DECISION FLOWCHART ║ ╠═══════════════════════════════════════════════════════════════════════════════╣ ║ ║ ║ START: Calculate DSCR ║ ║ │ ║ ║ ▼ ║ ║ ╔═══════════════════════════╗ ║ ║ ║ Is DSCR below 1.00? ║ ║ ║ ╚═══════════════════════════╝ ║ ║ │ │ ║ ║ YES NO ║ ║ │ │ ║ ║ ▼ ▼ ║ ║ ╔═════════════════╗ ╔═══════════════════════════╗ ║ ║ ║ DEFINITE REJECT ║ ║ Is DSCR 1.00 to 1.24? ║ ║ ║ ║ Do not submit ║ ╚═══════════════════════════╝ ║ ║ ╚═════════════════╝ │ │ ║ ║ YES NO ║ ║ │ │ ║ ║ ▼ ▼ ║ ║ ╔═════════════════╗ ╔═══════════════════════╗ ║ ║ ║ LIKELY REJECT ║ ║ Is DSCR 1.25 to 1.49? ║ ║ ║ ║ Improve first ║ ╚═══════════════════════╝ ║ ║ ╚═════════════════╝ │ │ ║ ║ YES NO ║ ║ │ │ ║ ║ ▼ ▼ ║ ║ ╔═════════════╗ ╔═════════════╗ ║ ║ ACCEPTABLE ║ ║ Is DSCR ║ ║ ║ May approve║ ║ 1.50 to 4.0?║ ║ ║ Expect ??? ║ ╚═════════════╝ ║ ╚═════════════╝ │ │ ║ YES NO ║ │ │ ║ ▼ ▼ ║ ╔═════════════╗ ╔═════════════╗ ║ ║ GOOD ║ ║ DSCR above ║ ║ ║ Approve ║ ║ 5.0? ║ ║ ║ Quickly ║ ╚═════════════╝ ║ ╚═════════════╝ │ │ ║ YES NO ║ │ │ ║ ▼ ▼ ║ ╔═════════════╗ ╔═════════════╗ ║ ║ SUSPICIOUS ║ ║ EXCELLENT ║ ║ ║ Under- ║ ║ Fast ║ ║ ║ borrowing ║ ║ Approval ║ ║ ║ Question ║ ║ ║ ║ ╚═════════════╝ ╚═════════════╝ ║ │ │ ║ └──────┬───────┘ ║ │ ║ ▼ ║ ╔═════════════════════╗ ║ ║ SUBMIT TO BANK ║ ║ ║ (with confidence) ║ ║ ╚═════════════════════╝ ║ │ ║ ▼ ║ ╔═════════════════════╗ ║ ║ LOAN APPROVED ║ ║ ╚═════════════════════╝ ║ │ ╚═══════════════════════════════════════════════════════════════════════════════╝

PART 11: WHERE TO PUT DSCR IN YOUR PROJECT REPORT

Your project report must include DSCR in these sections:

| Section | What to Include |

|---|---|

| Executive Summary (Page 1-2) | Year 1 DSCR (bold, clear) |

| Financial Projections (Page 8-11) | 5-year DSCR table |

| DSCR Calculation Page (Page 12) | Complete formula with step-by-step working |

| Loan Repayment Schedule | Monthly EMI table showing principal + interest |

| CMA Data / Key Ratios (Page 13) | DSCR year-by-year with other ratios |

Sample DSCR Page for Your Project Report

Your project report should have a dedicated page for DSCR. Here is what it should look like:

html

<h2>Debt Service Coverage Ratio (DSCR) Calculation</h2> <p><strong>DSCR Formula:</strong> (Net Profit + Depreciation + Interest on Term Loan) ÷ (Annual EMI)</p> <h3>Year 1 Calculation:</h3> | Component | Amount (₹) | |-----------|------------| | Net Profit After Tax | 68,575 | | Add: Depreciation | 7,000 | | Add: Interest on Term Loan | 20,425 | | Total Available for Debt Service | 96,000 | | Annual EMI (₹4,000 × 12) | 48,000 | | DSCR | 2.00 | <h3>5-Year DSCR Projection:</h3> | Year | Net Profit (₹) | Depreciation (₹) | Interest (₹) | Total (₹) | Annual EMI (₹) | DSCR | |------|---------------|-----------------|--------------|-----------|----------------|------| | 1 | 68,575 | 7,000 | 20,425 | 96,000 | 48,000 | 2.00 | | 2 | 89,037 | 6,300 | 17,463 | 1,12,800 | 48,000 | 2.35 | | 3 | 1,07,020 | 5,670 | 13,670 | 1,26,360 | 48,000 | 2.63 | | 4 | 1,21,221 | 5,103 | 9,205 | 1,35,529 | 48,000 | 2.82 | | 5 | 1,30,881 | 4,593 | 4,140 | 1,39,614 | 48,000 | 2.91 | <p><strong>Interpretation:</strong> DSCR improves every year. The business has strong repayment capacity. The minimum DSCR of 1.25 is met and exceeded in all years.</p>

👉 [See complete DSCR page in sample report – free PDF]

PART 12: COMPETITOR COMPARISON – DSCR IN THEIR REPORTS

| Feature | Finline | Sharda Associates | Fortrisk Consulting | MudraReady |

|---|---|---|---|---|

| DSCR Included? | Yes | Yes | Yes | Yes |

| DSCR Formula Shown? | No (hidden) | Sometimes | No | Yes (step by step) |

| 5-Year DSCR Table? | No | Yes | No | Yes |

| DSCR Interpretation? | No | Yes | No | Yes |

| Industry-Specific Examples? | No | Yes (limited) | No | Yes (10+ businesses) |

| Sensitivity Analysis with DSCR? | No | No | No | Yes (stress test) |

| Cost for Full Report | ₹499-999 | ₹2,000-10,000 | ₹399-2,499 | ₹399 |

| Time to Get Report | Same day | 3-5 days | 15 minutes-5 days | 30 minutes |

Why MudraReady is better for DSCR:

| Advantage | Explanation |

|---|---|

| Formula is shown | No hidden calculations. You can verify. |

| 5-year projection | Banks want to see trend, not just one year |

| Industry examples | 10+ business types with real numbers |

| Sensitivity analysis | Shows DSCR if sales drop 5-10% |

| Affordable | ₹399 vs CA ₹2,000-10,000 |

| Fast | 30 minutes vs CA 3-5 days |

👉 [Get your report with accurate DSCR – 30 minutes, ₹399 only]

PART 13: FREQUENTLY ASKED QUESTIONS (FAQ)

What is the minimum DSCR required for Mudra loan?

The minimum DSCR required is 1.25. Below 1.25, the bank will reject your application automatically. For Tarun Plus loans (₹10-20 lakh), banks often require 1.50 or higher.

What is the formula for DSCR in banking?

DSCR = (Net Profit After Tax + Depreciation + Interest on Term Loan) ÷ (Annual EMI)

Is DSCR mandatory for Mudra loan?

For Kishore, Tarun, and Tarun Plus loans, yes. For Shishu loans (up to ₹50,000), DSCR is not mandatory but a simple business plan helps.

How to increase DSCR?

Increase revenue projection, reduce expense projection, reduce loan amount, increase loan tenure, or negotiate lower interest rate.

Do I need to show DSCR for all 5 years?

Yes. Banks want to see DSCR improving over time. Year 1 may be lower, but Year 2, 3, 4, 5 should be higher.

Where can I get a project report with correct DSCR calculation?

MudraReady automatically calculates DSCR using the standard banking formula. No manual errors. ₹399 only.

What is a good DSCR for a new business?

For new businesses, Year 1 DSCR can be lower (1.10-1.25). Banks look at Year 2 and Year 3. If DSCR improves to 1.50+ by Year 2, approval chances are high.

How do banks verify DSCR?

Banks check your ITR (Income Tax Returns) and bank statements to verify if your actual profit matches the DSCR in your project report. Do not inflate numbers.

CONCLUSION – YOUR DSCR CHEAT SHEET

| DSCR Value | Meaning | Action |

|---|---|---|

| Below 1.00 | Cannot pay EMI | Do not submit. Fix urgently. |

| 1.00 – 1.24 | Weak – likely reject | Improve before submitting |

| 1.25 – 1.49 | Acceptable – may approve | Submit but expect questions |

| 1.50 – 2.00 | Good – likely approve | Submit confidently |

| 2.00 – 4.00 | Excellent – fast approval | Submit immediately |

| Above 5.00 | Suspicious – under-borrowing | Add explanation in report |

The single most important number in your project report is DSCR.

Get it right. Get your loan approved.

👉 Make your project report with correct DSCR calculation – 30 minutes, ₹399 only

RELATED GUIDES

- [How to Make a Project Report for Mudra Loan – 7 Step Guide] – Complete structure

- [Why Banks Reject Mudra Loans – 7 Reasons] – Avoid common mistakes

- [Mudra Loan Documents List 2026 – Complete Checklist] – All documents in one place

- [Kirana Store Project Report – Free Sample] – See DSCR in action

- [Candle Making Project Report – Free Sample] – Manufacturing business example

- [Tailoring Shop Project Report – Free Sample] – Small business example